Balanced scorecard

How should balanced scorecard be measured and interpreted?

Contents

The balanced scorecard (BSC) was developed by Kaplan and Norton in 1992 as an alternative to traditional performance measurement approaches that focus solely on.

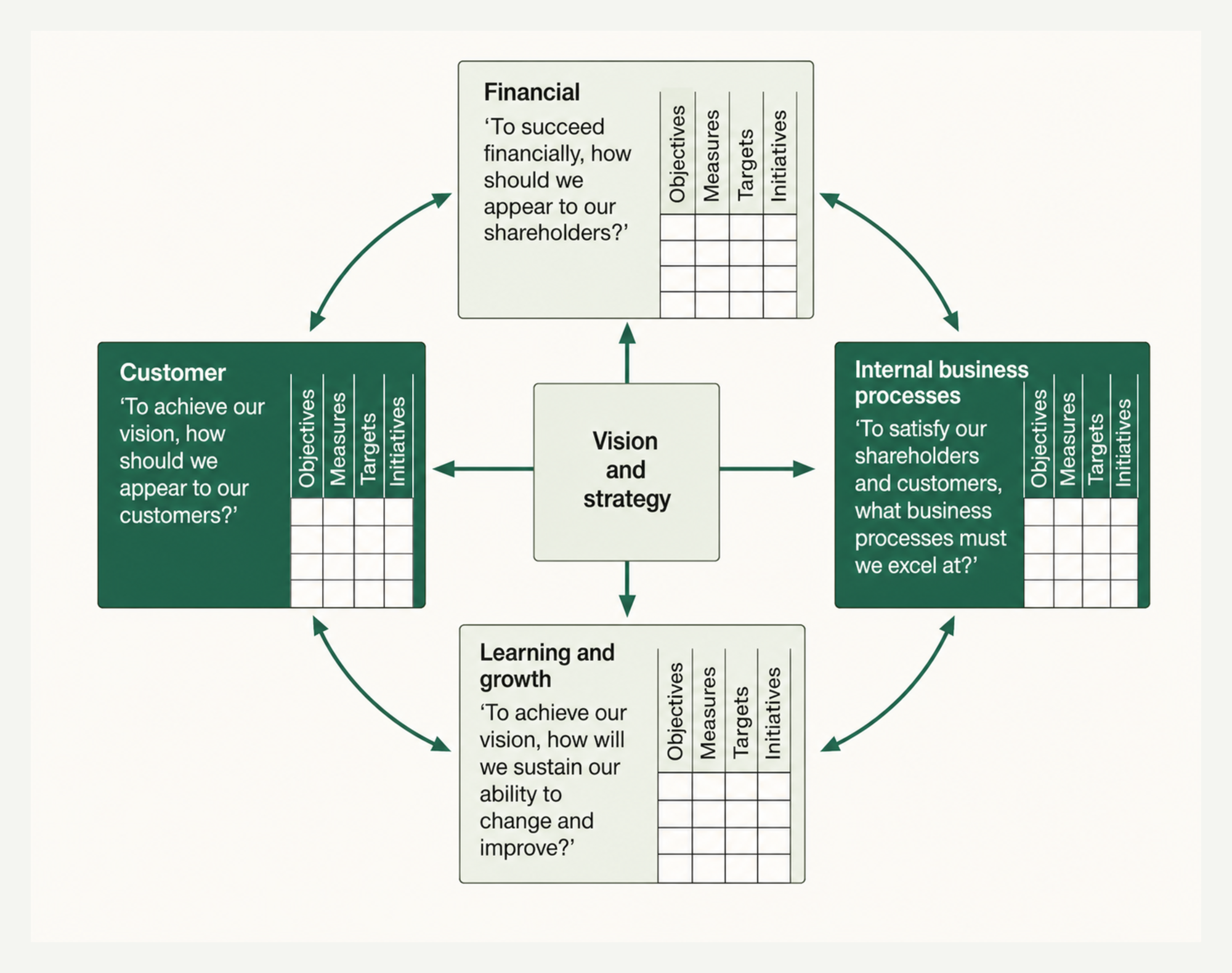

The balanced scorecard (BSC), introduced by Robert Kaplan and David Norton in 1992, broadened performance management beyond financial indicators that describe only past results. It translates an organisation’s mission, vision and strategy into objectives monitored across four perspectives. Relevant key performance indicators (KPIs) in each perspective make the long-term direction more concrete, allowing management to track execution and take corrective action promptly.

When to use it

Use the BSC when traditional financial reporting is too narrow to manage strategy. It complements financial outcomes with the non-financial drivers of future success across financial, internal business processes, learning and growth and customer perspectives. The scorecard asks:

- Which outcomes matter to shareholders?

- How do customers experience and perceive the organisation?

- Which internal processes create the greatest value?

- Does the organisation have the learning and innovation capacity required for the future?

The scorecard combines lagging indicators of past performance with current operating measures and leading indicators of future readiness. A transparent, multidimensional view helps managers see where execution is diverging from strategy and intervene in time to support durable performance improvement.

Origins

Kaplan and Norton developed the BSC through a multi-company research project and introduced it in their 1992 Harvard Business Review article “The Balanced Scorecard—Measures That Drive Performance.” Their work built on earlier performance dashboards, including the French tableau de bord, and on a corporate scorecard created at Analog Devices by Art Schneiderman. Kaplan and Norton subsequently expanded the concept from measurement into a system for translating and executing strategy.

What it is

The BSC expresses strategy as a connected set of objectives and measures across four perspectives: financial, customer, internal process, and learning and growth. Its logic is causal: people, information and capabilities enable stronger processes; stronger processes improve customer outcomes; and customer outcomes contribute to the intended financial results. A genuine scorecard is therefore a strategic hypothesis expressed through measures, not a collection of unrelated KPIs.

Continue your preview

Read more of Balanced scorecard.

Create a free account to continue this advanced article preview. Complete access is available with Pro or an eligible outcome pack, so you can see the value before deciding to upgrade.